Fill Your Michigan 2196 Template

Michigan PDF Forms

Fill Your Michigan 2196 Template

The Michigan 2196 form is essential for retailers and dealers seeking reimbursement for handling empty returnable containers. Alongside this form, several other documents may be necessary to ensure a complete submission and compliance with state regulations. Below is a list of commonly used forms and documents that complement the Michigan 2196 form.

Using these forms and documents in conjunction with the Michigan 2196 form can help streamline the reimbursement process and ensure compliance with state regulations. Always ensure that all information is accurate and submitted on time to avoid delays in processing your request.

Michigan Department of Treasury |

Report Year |

|

2196 (Rev. |

||

2012 |

||

|

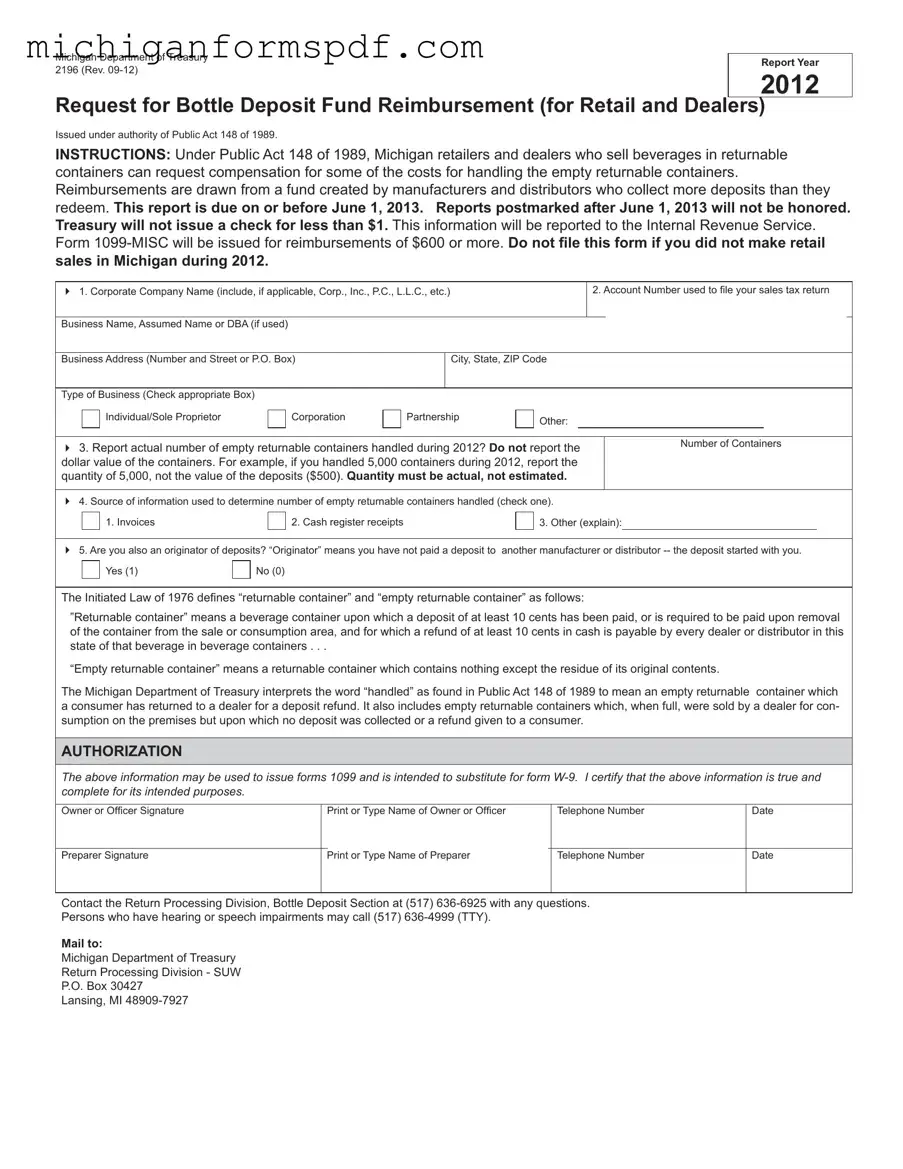

Request for Bottle Deposit Fund Reimbursement (for Retail and Dealers)

Issued under authority of Public Act 148 of 1989.

INSTRUCTIONS: Under Public Act 148 of 1989, Michigan retailers and dealers who sell beverages in returnable containers can request compensation for some of the costs for handling the empty returnable containers. Reimbursements are drawn from a fund created by manufacturers and distributors who collect more deposits than they redeem. This report is due on or before June 1, 2013. Reports postmarked after June 1, 2013 will not be honored. Treasury will not issue a check for less than $1. This information will be reported to the Internal Revenue Service. Form

1. Corporate Company Name (include, if applicable, Corp., Inc., P.C., L.L.C., etc.) |

|

|

|

|

2. Account Number used to fi le your sales tax return |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Business Name, Assumed Name or DBA (if used) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Business Address (Number and Street or P.O. Box) |

|

City, State, ZIP Code |

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Type of Business (Check appropriate Box) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Individual/Sole Proprietor |

|

|

Corporation |

|

|

Partnership |

|

|

Other: |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3. Report actual number of empty returnable containers handled during 2012? Do not report the |

|

|

Number of Containers |

||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||

dollar value of the containers. For example, if you handled 5,000 containers during 2012, report the |

|

|

|

|

|

|

|||||||||||||||

quantity of 5,000, not the value of the deposits ($500). Quantity must be actual, not estimated. |

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

4. Source of information used to determine number of empty returnable containers handled (check one). |

|

|

|

|

|

|

|||||||||||||||

|

|

1. Invoices |

|

|

2. Cash register receipts |

|

|

|

|

3. Other (explain): |

|

|

|||||||||

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

||||||||||||||||

5. Are you also an originator of deposits? “Originator” means you have not paid a deposit to |

another manufacturer or distributor |

||||||||||||||||||||

|

|

Yes (1) |

|

|

No (0) |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

The Initiated Law of 1976 defi nes “returnable container” and “empty returnable container” as follows:

”Returnable container” means a beverage container upon which a deposit of at least 10 cents has been paid, or is required to be paid upon removal of the container from the sale or consumption area, and for which a refund of at least 10 cents in cash is payable by every dealer or distributor in this state of that beverage in beverage containers . . .

“Empty returnable container” means a returnable container which contains nothing except the residue of its original contents.

The Michigan Department of Treasury interprets the word “handled” as found in Public Act 148 of 1989 to mean an empty returnable container which a consumer has returned to a dealer for a deposit refund. It also includes empty returnable containers which, when full, were sold by a dealer for con- sumption on the premises but upon which no deposit was collected or a refund given to a consumer.

AUTHORIZATION

The above information may be used to issue forms 1099 and is intended to substitute for form

Owner or Offi cer Signature |

|

Print or Type Name of Owner or Officer |

|

Telephone Number |

Date |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer Signature |

|

Print or Type Name of Preparer |

|

Telephone Number |

Date |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Contact the Return Processing Division, Bottle Deposit Section at (517)

Persons who have hearing or speech impairments may call (517)

Mail to:

Michigan Department of Treasury

Return Processing Division - SUW

P.O. Box 30427

Lansing, MI

Bottle Deposit Fund Reimbursement Availability

INSTRUCTIONS: Under Public Act 148 of 1989, Michigan retailers and dealers who sell beverages in returnable containers can request compensation for some of the costs for handling the empty returnable containers.

Reimbursements are drawn from a fund created by manufacturers and distributors who collect more deposits than they redeem.

The payment is based on the number of empty returnable containers handled in a calendar year. Payment amounts will be known after Treasury determines how much money is available.

To apply, you must complete and mail a Request for Bottle Deposit Fund Reimbursement (Form 2196) to Treasury. Form 2196 is due on or before June 1, 2013. Use Form 2196 or contact Return Processing Division, Bottle Deposit Section, at (517)

Treasury will begin issuing checks after August 1.

IRS Form 1099-MISC: This form is used to report various types of income other than wages, salaries, and tips. Similar to the Michigan 2196 form, it is essential for documenting reimbursements that exceed $600. Both forms require accurate reporting of financial transactions to ensure compliance with tax regulations.

Michigan Sales Tax Return (Form 5080): Retailers must file this form to report sales tax collected from customers. Like the Michigan 2196, it involves detailed reporting of financial data, including account numbers and business information. Both forms serve to ensure that businesses are accountable for their financial activities.

Michigan Corporate Income Tax (CIT) Form: This form is used by corporations to report their income and calculate tax liability. Similar to the Michigan 2196, it requires businesses to provide specific details about their operations and financial transactions, ensuring transparency and compliance with state regulations.

Form W-9: This form is used to provide taxpayer identification information to entities that will report payments made to an individual or business. Like the Michigan 2196, it serves as a certification of accuracy regarding the information provided, and both are crucial for tax reporting purposes.

Michigan Subpoena Form - Judicial officers can express their intent through this form, maintaining order and structure.

A Georgia Hold Harmless Agreement is a legal document designed to protect one party from liability for potential damages or injuries that may occur during a specified activity or event. This form establishes a mutual understanding between the parties involved, ensuring that one party will not hold the other responsible for certain risks. By utilizing this agreement, individuals and organizations can promote safer interactions while clearly outlining their responsibilities, as recommended by Forms Georgia.

2022 Michigan Tax Forms - If you're filing for a fiduciary, specific lines within the form apply differently.

Understanding the Michigan 2196 form is essential for retailers and dealers who sell beverages in returnable containers. However, several misconceptions surround this form. Here are ten common misunderstandings:

By clarifying these misconceptions, retailers and dealers can better navigate the process of applying for reimbursements under the Michigan 2196 form.

Completing the Michigan 2196 form is an essential step for retailers and dealers seeking reimbursement for handling empty returnable containers. Following the outlined steps will ensure that the form is filled out correctly and submitted on time.

After completing the form, it is important to mail it to the Michigan Department of Treasury by the specified deadline. Ensure that it is postmarked on or before June 1, 2013, to be considered for reimbursement. For any questions or additional information, contact the Return Processing Division, Bottle Deposit Section.

When filling out the Michigan 2196 form, there are important actions to take and avoid to ensure your application is processed smoothly. Below is a list of things you should and shouldn't do: