Fill Your Michigan 5092 Template

Michigan PDF Forms

Fill Your Michigan 5092 Template

The Michigan 5092 form is essential for amending sales, use, and withholding taxes. When filing this form, several other documents may also be required to ensure compliance and accuracy. Below is a list of commonly used forms and documents that often accompany the Michigan 5092.

Understanding these associated documents can streamline the amendment process and help ensure compliance with Michigan tax regulations. Properly completing the Michigan 5092 form along with the necessary accompanying documents can prevent future complications and penalties.

Michigan Department of Treasury 5092

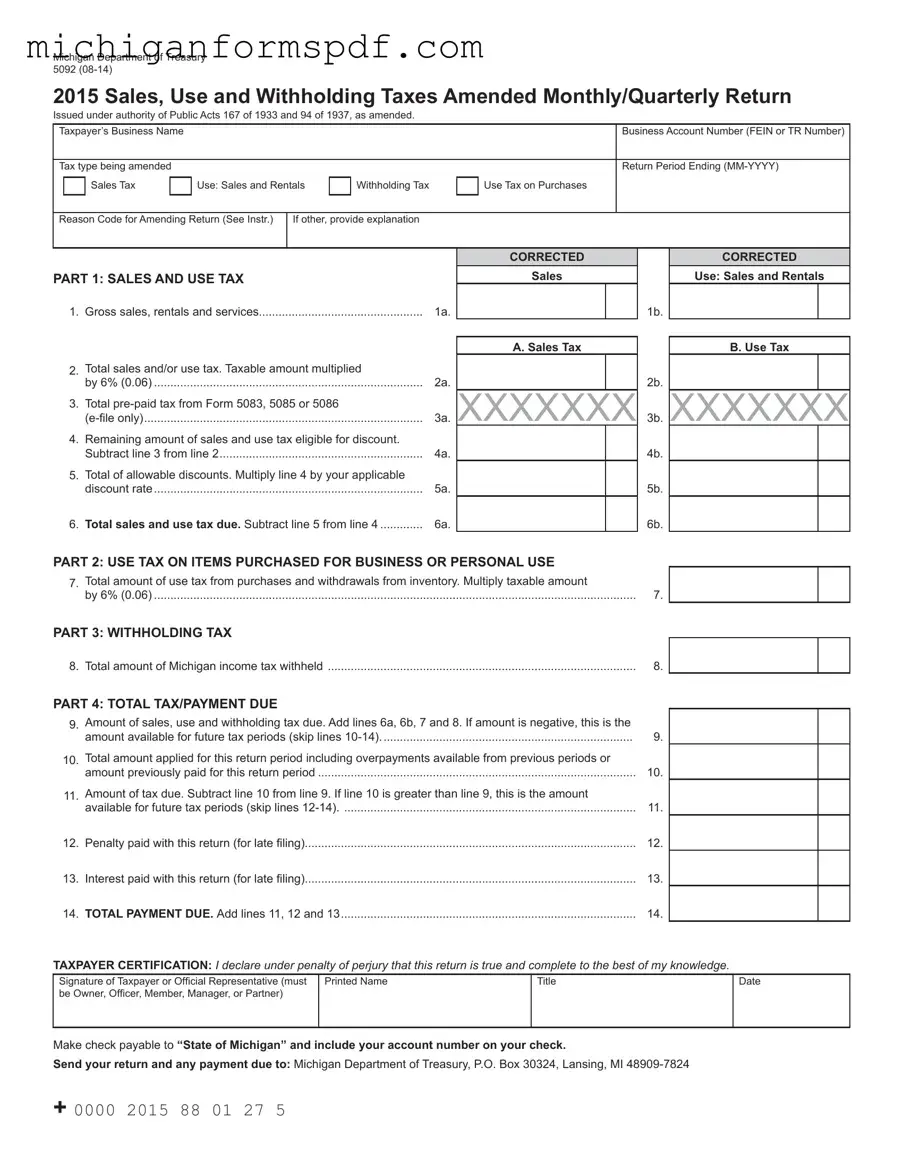

2015 Sales, Use and Withholding Taxes Amended Monthly/Quarterly Return

Issued under authority of Public Acts 167 of 1933 and 94 of 1937, as amended.

Taxpayer’s Business Name |

|

|

|

|

|

Business Account Number (FEIN or TR Number) |

|||

|

|

|

|

|

|

|

|

|

|

Tax type being amended |

|

|

|

|

|

Return Period Ending |

|||

|

|

|

|

|

|

|

|

|

|

|

|

Sales Tax |

|

Use: Sales and Rentals |

|

Withholding Tax |

|

Use Tax on Purchases |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Reason Code for Amending Return (See Instr.)

If other, provide explanation

PART 1: SAlES AnD USE TAx

1. Gross sales, rentals and services |

1a. |

CORRECTED

Sales

1b.

CORRECTED

Use: Sales and Rentals

2.Total sales and/or use tax. Taxable amount multiplied

by 6% (0.06) ..................................................................................

3.Total

4.Remaining amount of sales and use tax eligible for discount. Subtract line 3 from line 2..............................................................

5.Total of allowable discounts. Multiply line 4 by your applicable discount rate..................................................................................

6.Total sales and use tax due. Subtract line 5 from line 4 .............

2a.

3a.

4a.

5a.

6a.

A. Sales Tax

XXXXXXX

2b.

3b.

4b.

5b.

6b.

B. Use Tax

XXXXXXX

PART 2: USE TAx On ITEMS PURChASED fOR BUSInESS OR PERSOnAl USE

7. Total amount of use tax from purchases and withdrawals from inventory. Multiply taxable amount |

|

by 6% (0.06) |

7. |

PART 3: WIThhOlDIng TAx

8. Total amount of Michigan income tax withheld |

8. |

PART 4: TOTAl TAx/PAyMEnT DUE

9. |

Amount of sales, use and withholding tax due. Add lines 6a, 6b, 7 and 8. If amount is negative, this is the |

|

|

amount available for future tax periods (skip lines |

9. |

10. |

Total amount applied for this return period including overpayments available from previous periods or |

|

|

amount previously paid for this return period |

10. |

11. |

Amount of tax due. Subtract line 10 from line 9. If line 10 is greater than line 9, this is the amount |

|

|

available for future tax periods (skip lines |

11. |

12. |

Penalty paid with this return (for late iling) |

12. |

13. |

Interest paid with this return (for late iling) |

13. |

14. |

TOTAl PAyMEnT DUE. Add lines 11, 12 and 13 |

14. |

TAxPAyER CERTIfICATIOn: I declare under penalty of perjury that this return is true and complete to the best of my knowledge.

Signature of Taxpayer or Oficial Representative (must be Owner, Oficer, Member, Manager, or Partner)

Printed Name

Title

Date

Make check payable to “State of Michigan” and include your account number on your check.

Send your return and any payment due to: Michigan Department of Treasury, P.O. Box 30324, Lansing, MI

+ 0000 2015 88 01 27 5

Instructions for Sales, Use and Withholding Taxes Amended Monthly/Quarterly Return (form 5092)

NOTE: You must use Form 165 to amend tax years prior to 2015.

Form 5092 is used to amend monthly/quarterly periods in the current year. Complete the return with the corrected figures. Check the box for each tax type you are amending and provide the amended reason code located in the instructions. If the reason code is “Other,” write an explanation for the amendment.

IMPORTANT: This is a return for Sales Tax, Use Tax, and/ or Withholding Tax. If the taxpayer inserts a zero on (or leaves blank) any line for reporting Sales Tax, Use Tax, or Withholding Tax, the taxpayer is certifying that no tax is owed for that tax type. If it is determined that tax is owed, the taxpayer will be liable for the deficiency as well as penalty and interest.

Reason code for amending return: Using the table below, select the

01Increasing tax liability

02Decreasing tax liability

03Incorrect information/igures reported on original return

04Original return was missing information/incomplete

05Claiming previously unclaimed

06Dispute an adjustment

07Tax Exempt

08Other

PART 1: SAlES AnD USE TAx

Line 1a: Total gross sales for tax period being reported. Enter the total of your Michigan sales of tangible personal property including cash, credit and installment transactions and any costs incurred before ownership of the property is transferred to the buyer (including shipping, handling, and delivery charges).

Line 1b: This line is used to report the following:

•

•Lessors of tangible personal property: Enter amount of total rental receipts.

•Persons providing accommodations: This would include but not limited to hotel, motel, and vacation home rentals. This also includes assessments imposed under the Convention and Tourism Act, the Convention Facility Development Act, the Regional Tourism Marketing Act, the Community Convention or Tourism Marketing Act.

•Telecommunications Services: Enter gross income from telecommunications services.

Line 2a: Total sales tax. Negative figures are not allowed or valid.

Line 2b: Total use tax. Negative figures not allowed or valid.

Line 5: Enter total allowable discounts. Discounts apply only to 2/3 (0.6667) of the sales and/or use tax collected at the 6 percent tax rate. See below to calculate your discount based on filing frequency:

Monthly Filer

•If the tax is less than $9, calculate the discount by multiplying the tax by 2/3 (.6667).

•Enter $6 if tax is $9 to $1,200 and paid by the 12th, or $9 to $1,800 and paid by the 20th .

•If the tax is more than $1,200 and paid by the 12th,

calculate discount using this formula: (Tax x .6667 x .0075). The maximum discount is $20,000 for the tax period.

•If the tax is more than $1,800 and paid by the 20th,

calculate discount using this formula: (Tax x .6667 x .005). The maximum discount is $15,000 for the tax period.

Quarterly Filer

•If the tax is less than $27, calculate the discount by multiplying the tax by 2/3 (.6667)

•Enter $18 if tax is $27 to $3,600 and paid by the 12th, or $27 to $5,400 and paid by the 20th.

•If the tax is more than $3,600 and paid by the 12th,

calculate discount using this formula: (Tax x .6667 x .0075). The maximum discount is $20,000 for the tax period.

•If the tax is more than $5,400 and paid by the 20th,

calculate discount using this formula: (Tax x .6667 x .005). The maximum discount is $15,000 for the tax period.

Accelerated Filer

•If the tax is paid by the 12th, calculate discount using this formula: (Tax x .6667 x .0075).

•If the tax is paid by the 20th, calculate discount using this formula: (Tax x .6667 x .005).

PART 2: USE TAx On ITEMS PURChASED fOR BUSInESS OR PERSOnAl USE

Line 7: To determine your use tax due from purchases and withdrawals, multiply the total amount of your inventory value by 6% (0.06) and enter here.

PART 3: WIThhOlDIng TAx

Line 8: Enter the total Michigan income tax withheld for the tax period.

PART 4: TOTAl TAx/PAyMEnT DUE

Line 9: If amount is negative, this is the amount available for

future tax periods (skip lines

Line 10: Enter any payments you submitted for this period, enter any payments for this period including any overpayments available from previous periods. If you are using an overpayment from a previous period only enter the amount needed to pay the total liability for this return. In the event an overpayment still exists declare it on the next return you file with a liability. (Liability minus overpayments/prior payment for this period must be greater than or equal to zero).

how to Compute Penalty and Interest

If your return is filed with additional tax due, include penalty and interest with your payment. Penalty is 5% of the tax due and increases by an additional 5% per month or fraction thereof, after the second month, to a maximum of 25%. Interest is charged daily using the average prime rate, plus 1 percent.

Refer to www.michigan.gov/taxes for current interest rate information or help in calculating late payment fees.

IRS Form 1040X: This is the U.S. Individual Income Tax Return Amended. Like the Michigan 5092, it allows taxpayers to correct errors on previously filed returns, ensuring accurate tax liability reporting.

IRS Form 941-X: This form is used to amend the Employer's Quarterly Federal Tax Return. Similar to the 5092, it helps correct mistakes in previously reported employment taxes.

Bill of Sale: A Bill of Sale form is essential for documenting the transfer of ownership of personal property, ensuring legality and transparency in transactions.

Michigan Form 5083: This is a Prepaid Sales Tax Return. It shares similarities with the 5092 in that both forms deal with sales tax, allowing for corrections and adjustments to previous filings.

IRS Form 1065: This is the U.S. Return of Partnership Income. If amended, it resembles the 5092 by allowing partnerships to correct income, deductions, and credits.

IRS Form 1120X: This is the Amended U.S. Corporation Income Tax Return. Like the 5092, it permits corporations to rectify previously filed tax returns.

Michigan Form 5018: This is the Michigan Corporate Income Tax Amended Return. Similar to the 5092, it allows corporations to amend their tax obligations.

IRS Form 990: This is the Return of Organization Exempt from Income Tax. When amended, it parallels the 5092 by enabling non-profits to correct financial information.

Michigan Form 4906: This is the Michigan Individual Income Tax Return Amended. It shares the purpose of correcting errors in individual tax filings, similar to the 5092.

IRS Form 8862: This is used to claim the Earned Income Credit after disallowance. It allows taxpayers to amend their claims, akin to how the 5092 corrects tax liabilities.

IRS Form 8863: This form is for Education Credits. When amended, it functions similarly to the 5092 by allowing taxpayers to correct education-related tax credits.

Michigan Permit - An existing hours deviation from Michigan Wage and Hour Division must be documented if applicable.

Divorce Forms Michigan - It may also require additional forms for child support or custody issues.

The Georgia Motor Vehicle Bill of Sale form is an important document used to record the transfer of ownership for a vehicle in Georgia. This form provides both the buyer and seller with proof of the transaction, helping to ensure a smooth transfer process. For those looking to access this form, you can easily find it on Forms Georgia, making the process of filling it out straightforward and efficient.

How Long Does It Take to Get a Birth Certificate in Michigan - Including correct and timely documentation is crucial for successful applications.

Understanding the Michigan 5092 form can be challenging, and several misconceptions may lead to confusion. Here are eight common misunderstandings about this form:

Being aware of these misconceptions can help ensure accurate and timely filing of the Michigan 5092 form, ultimately avoiding unnecessary penalties and interest.

Completing the Michigan 5092 form requires careful attention to detail. This form is essential for amending your sales, use, and withholding taxes for a specific period. After filling out the form correctly, you will need to submit it along with any payment due to the Michigan Department of Treasury.

When filling out the Michigan 5092 form, attention to detail is crucial. Here are some important do's and don'ts to keep in mind:

By following these guidelines, you can help ensure that your submission is processed smoothly and accurately. Always double-check your work before submitting the form.