Fill Your Michigan 777 Template

Michigan PDF Forms

Fill Your Michigan 777 Template

The Michigan 777 form is an important document for residents who have income taxed by a Canadian province. It allows taxpayers to claim a credit for taxes paid to Canada, helping to avoid double taxation. Alongside the Michigan 777 form, there are several other forms and documents that are commonly used in conjunction with it. Below is a brief overview of these related forms.

Understanding these forms and how they interact with the Michigan 777 can simplify the tax filing process for individuals with Canadian income. Each document plays a crucial role in ensuring taxpayers maximize their credits and comply with both state and federal tax regulations.

Michigan Department of Treasury, ITD

777 (Rev.

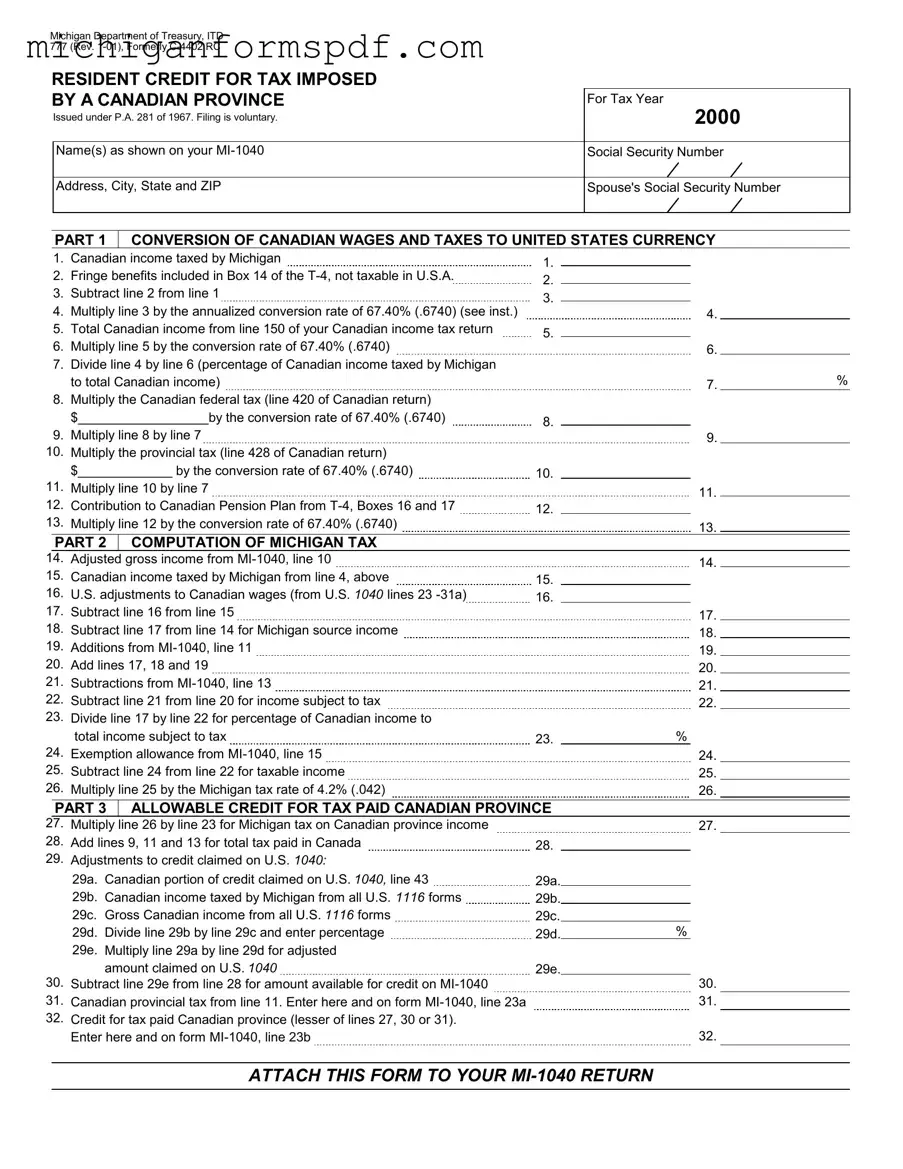

RESIDENT CREDIT FOR TAX IMPOSED |

|

|

|

BY A CANADIAN PROVINCE |

For Tax Year |

Issued under P.A. 281 of 1967. Filing is voluntary. |

2000 |

|

|

Name(s) as shown on your |

Social Security Number |

|

|

Address, City, State and ZIP |

Spouse's Social Security Number |

|

|

PART 1

CONVERSION OF CANADIAN WAGES AND TAXES TO UNITED STATES CURRENCY

1. |

Canadian income taxed by Michigan |

1. |

|

|

|

2. |

Fringe benefits included in Box 14 of the |

2. |

|

|

|

3. |

Subtract line 2 from line 1 |

3. |

|

|

|

4. |

Multiply line 3 by the annualized conversion rate of 67.40% (.6740) (see inst.) |

|

5. |

Total Canadian income from line 150 of your Canadian income tax return |

5. |

|

|

6.Multiply line 5 by the conversion rate of 67.40% (.6740)

7.Divide line 4 by line 6 (percentage of Canadian income taxed by Michigan to total Canadian income)

8.Multiply the Canadian federal tax (line 420 of Canadian return)

|

$__________________by the conversion rate of 67.40% (.6740) |

8. |

|

|

|

9. |

Multiply line 8 by line 7 |

|

10. |

Multiply the provincial tax (line 428 of Canadian return) |

|

|

$_____________ by the conversion rate of 67.40% (.6740) |

10. |

11. |

Multiply line 10 by line 7 |

|

12. |

Contribution to Canadian Pension Plan from |

12. |

13. |

Multiply line 12 by the conversion rate of 67.40% (.6740) |

|

4.

6.

7.%

11.

13.

PART 2 COMPUTATION OF MICHIGAN TAX

14.Adjusted gross income from

15.Canadian income taxed by Michigan from line 4, above

16.U.S. adjustments to Canadian wages (from U.S. 1040 lines 23

17.Subtract line 16 from line 15

18.Subtract line 17 from line 14 for Michigan source income

19.Additions from

20.Add lines 17, 18 and 19

21.Subtractions from

22.Subtract line 21 from line 20 for income subject to tax

23.Divide line 17 by line 22 for percentage of Canadian income to

total income subject to tax

24.Exemption allowance from

25.Subtract line 24 from line 22 for taxable income

26.Multiply line 25 by the Michigan tax rate of 4.2% (.042)

14.

15.

16.

17.

18.

19.

20.

21.

22.

23.%

24.

25.

26.

PART 3 ALLOWABLE CREDIT FOR TAX PAID CANADIAN PROVINCE

27. |

Multiply line 26 by line 23 for Michigan tax on Canadian province income |

|

|

28. |

Add lines 9, 11 and 13 for total tax paid in Canada |

28. |

|

29. |

Adjustments to credit claimed on U.S. 1040: |

|

|

|

29a. |

Canadian portion of credit claimed on U.S. 1040, line 43 |

29a. |

|

29b. |

Canadian income taxed by Michigan from all U.S. 1116 forms |

29b. |

|

29c. |

Gross Canadian income from all U.S. 1116 forms |

29c. |

|

29d. |

Divide line 29b by line 29c and enter percentage |

29d. |

|

29e. |

Multiply line 29a by line 29d for adjusted |

|

|

|

amount claimed on U.S. 1040 |

29e. |

30.Subtract line 29e from line 28 for amount available for credit on

31.Canadian provincial tax from line 11. Enter here and on form

32.Credit for tax paid Canadian province (lesser of lines 27, 30 or 31). Enter here and on form

27.

%

30.

31.

32.

ATTACH THIS FORM TO YOUR

The Michigan 777 form is a specific document used for claiming a resident credit for taxes imposed by a Canadian province. It shares similarities with several other tax-related documents, each serving unique purposes but often addressing similar financial concerns. Here are four documents that are comparable to the Michigan 777 form:

Michigan Tax Return Form - The Michigan Department of Treasury oversees the forms related to real estate transfers.

When entering into a financial agreement, it's essential to use the correct documentation to protect both the lender and the borrower, and a New Jersey Promissory Note serves this purpose effectively. By utilizing this legal form, both parties can establish clear terms regarding repayment timelines and interest obligations, minimizing the risk of misunderstandings. To create your own promissory note, you can find a suitable template at https://promissoryform.com/blank-new-jersey-promissory-note/.

Michigan Nonprofit - Changes to the organization's charitable purposes must be summarized in 50 words or less.

The Michigan 777 form, also known as the Resident Credit for Tax Imposed by a Canadian Province, can often be misunderstood. Here are ten common misconceptions about this form:

Understanding these misconceptions can help taxpayers navigate the complexities of the Michigan 777 form more effectively. It’s always best to consult with a tax professional if there are any uncertainties.

Filling out the Michigan 777 form requires careful attention to detail. This form is used to report and claim a credit for taxes paid to a Canadian province. Ensure that all information is accurate and complete before submitting it with your MI-1040 return.

Next, proceed to Part 1, which focuses on converting Canadian wages and taxes to U.S. currency.

Now move to Part 2, which is focused on the computation of Michigan tax.

Finally, proceed to Part 3 to calculate the allowable credit for tax paid to a Canadian province.

Ensure to attach this form to your MI-1040 return before submission.

When filling out the Michigan 777 form, it is essential to follow specific guidelines to ensure accuracy and compliance. Here are some important dos and don'ts to consider: