Fill Your Michigan 807 Template

Michigan PDF Forms

Fill Your Michigan 807 Template

The Michigan 807 form is a key document for partnerships, S corporations, and other flow-through entities filing their composite individual income tax returns. However, it is not the only form you'll need. There are several other documents that often accompany the Michigan 807 form, each serving a specific purpose in the tax filing process. Here’s a brief overview of these essential forms and documents.

Understanding these accompanying documents is vital for ensuring a smooth tax filing process. Each form plays a unique role in providing necessary information to the Michigan Department of Treasury, and together they help clarify the financial standing of the partnership or S corporation. Properly completing and submitting these forms can help avoid penalties and ensure compliance with state tax laws.

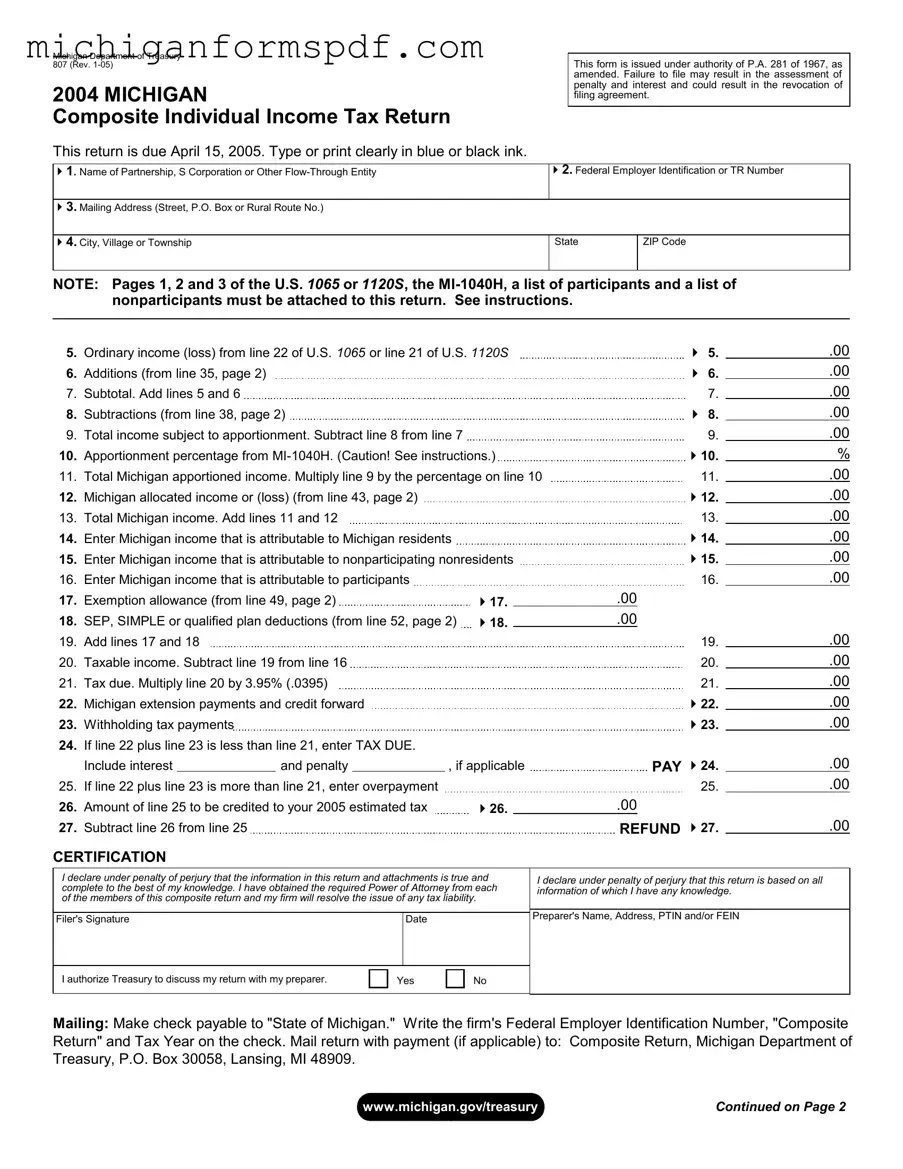

Michigan Department of Treasury 807 (Rev.

2004 MICHIGAN

Composite Individual Income Tax Return

This return is due April 15, 2005. Type or print clearly in blue or black ink.

This form is issued under authority of P.A. 281 of 1967, as amended. Failure to file may result in the assessment of penalty and interest and could result in the revocation of filing agreement.

1. Name of Partnership, S Corporation or Other |

2. Federal Employer Identification or TR Number |

|

|

|

|

3. Mailing Address (Street, P.O. Box or Rural Route No.) |

|

|

|

|

|

4. City, Village or Township |

State |

ZIP Code |

|

|

|

NOTE: Pages 1, 2 and 3 of the U.S. 1065 or 1120S, the

5. |

Ordinary income (loss) from line 22 of U.S. 1065 or line 21 of U.S. 1120S |

|

5. |

.00 |

||

6. |

Additions (from line 35, page 2) |

|

|

|

6. |

.00 |

7. |

Subtotal. Add lines 5 and 6 |

|

|

7. |

.00 |

|

8. |

Subtractions (from line 38, page 2) |

|

|

|

8. |

.00 |

9. |

Total income subject to apportionment. Subtract line 8 from line 7 |

|

|

9. |

.00 |

|

10. |

Apportionment percentage from |

|

10. |

% |

||

11. |

Total Michigan apportioned income. Multiply line 9 by the percentage on line 10 |

11. |

.00 |

|||

12. |

Michigan allocated income or (loss) (from line 43, page 2) |

|

|

|

12. |

.00 |

13. |

Total Michigan income. Add lines 11 and 12 |

|

|

13. |

.00 |

|

14. |

Enter Michigan income that is attributable to Michigan residents |

|

|

|

14. |

.00 |

15. |

Enter Michigan income that is attributable to nonparticipating nonresidents |

|

15. |

.00 |

||

16. |

Enter Michigan income that is attributable to participants |

|

|

16. |

.00 |

|

17. |

Exemption allowance (from line 49, page 2) |

17. |

|

.00 |

|

|

18. |

SEP, SIMPLE or qualified plan deductions (from line 52, page 2) |

18. |

|

.00 |

|

|

|

19. |

.00 |

||||

19. |

Add lines 17 and 18 |

|

|

|||

20. |

Taxable income. Subtract line 19 from line 16 |

|

|

20. |

.00 |

|

21. |

Tax due. Multiply line 20 by 3.95% (.0395) |

|

|

21. |

.00 |

|

22. |

Michigan extension payments and credit forward |

|

|

|

22. |

.00 |

23. |

Withholding tax payments |

|

|

|

23. |

.00 |

24.If line 22 plus line 23 is less than line 21, enter TAX DUE.

|

Include interest |

|

and penalty |

|

, if applicable |

|

PAY 24. |

.00 |

|

|

|

|

|

.00 |

|||||

25. |

If line 22 plus line 23 is more than line 21, enter overpayment |

|

|

25. |

|||||

26. |

Amount of line 25 to be credited to your 2005 estimated tax |

26. |

|

.00 |

|

|

|||

27. |

Subtract line 26 from line 25 |

|

|

|

|

REFUND 27. |

.00 |

||

|

|

|

|

|

|||||

CERTIFICATION

I declare under penalty of perjury that the information in this return and attachments is true and |

I declare under penalty of perjury that this return is based on all |

||||||

complete to the best of my knowledge. I have obtained the required Power of Attorney from each |

|||||||

information of which I have any knowledge. |

|||||||

of the members of this composite return and my firm will resolve the issue of any tax liability. |

|||||||

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer's Name, Address, PTIN and/or FEIN |

|

Filer's Signature |

|

|

Date |

|

|

||

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

I authorize Treasury to discuss my return with my preparer. |

|

Yes |

|

No |

|

||

|

|

|

|||||

|

|

|

|

|

|

|

|

Mailing: Make check payable to "State of Michigan." Write the firm's Federal Employer Identification Number, "Composite

Return" and Tax Year on the check. Mail return with payment (if applicable) to: Composite Return, Michigan Department of Treasury, P.O. Box 30058, Lansing, MI 48909.

www.michigan.gov/treasury |

Continued on Page 2 |

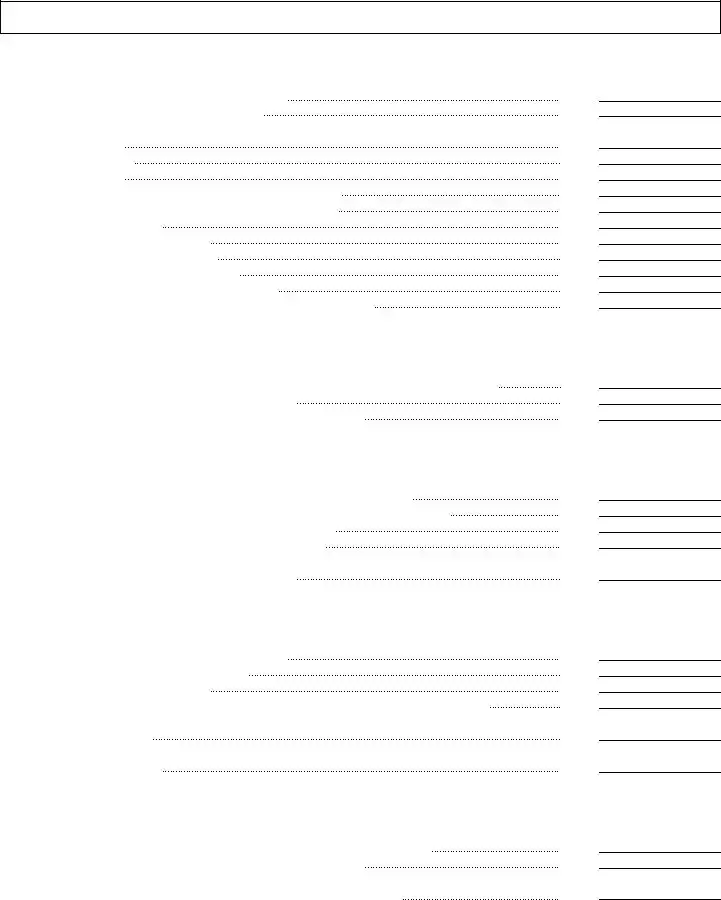

2004 807, Page 2

Name of Partnership, S Corporation or Other Flow Through Entity |

Federal Employer Identification or TR Number |

|

|

|

ADDITIONS (see instructions) |

|

28. |

Net income (loss) from rental real estate activities |

28. |

29. |

Net income (loss) from other rental activities |

29. |

30. |

Portfolio Income (loss) (see instructions): |

|

|

a. Interest income |

30a. |

|

b. Dividend income |

30b. |

|

c. Royalty income |

30c. |

|

d. Net |

30d. |

|

e. Net |

30e. |

|

f. Other portfolio income |

30f. |

31. |

Net gain (loss) under Section 1231 |

31. |

32. |

Other income from U.S. Schedule K |

32. |

33. |

State or local taxes measured by income |

33. |

34. |

Other miscellaneous additions (attach schedule) |

34. |

35. |

Total additions. Add lines 28 through 34. Enter here and on line 6 |

35. |

|

SUBTRACTIONS (see instructions) |

|

36. |

Income (loss) from other partnerships, S corp. and fiduciaries included in ordinary income |

36. |

37. |

Other miscellaneous subtractions (attach schedule) |

37. |

38. |

Total subtractions. Add lines 36 and 37. Enter here and on line 8 |

38. |

|

MICHIGAN ALLOCATED INCOME OR (LOSS) |

|

39. |

Guaranteed payments to participants for services performed in Michigan |

39. |

40. |

Income attributable to other Michigan partnerships, S corporations or fiduciaries |

40. |

41. |

Net Michigan capital gains (losses) (from U.S. Schedule D) |

41. |

42. |

Other Michigan allocated income (loss) (see instructions) |

42. |

43. |

Total Michigan allocated income (loss). |

|

|

Add lines 39 through 42. Enter here and on line 12 |

43. |

|

EXEMPTION ALLOWANCE |

|

44. |

Number of participants included in this agreement |

44. |

45. |

Line 44 times $3,100 exemption allowance |

45. |

46. |

Total Michigan income from line 13 |

46. |

47. |

Total distributive income (Total Distributive Income from Distributive Income Worksheet) |

47. |

48. |

Percent of income attributable to Michigan. Divide line 46 by line 47. |

|

|

(May not exceed 100%.) |

48. |

49. |

Apportioned exemption allowance. Multiply line 45 by the percentage on line 48 |

|

|

Enter here and on line 17 |

49. |

|

SEP, SIMPLE OR QUALIFIED PLAN SUBTRACTIONS |

|

50. |

SEP, SIMPLE or qualified plan subtractions for participants (attach schedule) |

50. |

51. |

Enter the percent of income attributable to Michigan from line 48 |

51. |

52. |

SEP, SIMPLE or qualified plan subtractions attributable to Michigan |

|

|

Multiply line 50 by the percentage on line 51. Enter here and on line 18 |

52. |

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

.00

%

.00

.00

%

.00

2004 807, PAGE 3

Instructions for Form 807, Michigan Composite Individual Income Tax Return

GENERAL INSTRUCTIONS

Who may file a return

A

Participation Requirements

A member may not participate in this composite return in any of the following cases:

•If he or she is claiming a city income tax credit, public contribution credit, community foundation credit, homeless shelter/food bank credit, college tuition credit or Michigan Historic Preservation Tax Credit.

•If he or she was a Michigan resident

•If he or she wishes to claim more than one Michigan exemption.

Due date of return

The composite return for any tax periods ending in 2004 is due April 15, 2005. The returns for any periods ending in 2005 will be due April 15, 2006.

If the firm cannot file by the due date, a request for an extension can be filed before the original due date. See “Requesting an Extension” on this page.

Withholding tax payments

Composite filers are required to make withholding tax payments on behalf of

all nonresident members (both participating and nonparticipating). The payment of withholding is due quarterly on April 20, July 20, and October 20 of the taxable year and January 20 of the succeeding year. The payment of withholding taxes is remitted on the payment voucher Form 160, Combined Return for Michigan Taxes.

Requesting an extension

The firm may request an extension of time to file by sending payment of the estimated annual liability to Treasury with a copy of an approved federal extension. Any extension allowed by the

Internal Revenue Service for filing the firm’s federal return automatically extends the due date of the composite return to the same extended due date.

If the firm does not apply for a federal extension, request an Application for Extension of Time to File Michigan Tax Returns (Form 4). When completing the extension form, check “Fiduciary Tax” in box 1, use the firm’s name and federal employer identification number (FEIN) and write “composite return” on the form. Follow these special instructions to make sure your account is credited properly.

Payment of the estimated annual liability

must be made with the extension application. When you file your composite return, attach a copy of your extension application to it. Obtain Form

from www.michigan.gov/treasury, Fiduciary Forms. Download a copy of the quarterly forms and complete one quarterly form. Use the name of the firm and the firm’s FEIN or the recipients Social Security number (SSN). Check the box labeled “CF” at the top of the voucher. Do not use the other three quarterly estimate forms.

Mailing refunds, assessments and correspondence

By signing the Michigan Composite Income Tax Return (Form 807), the signing partner or officer declares that the firm has power of attorney from each participant to file a composite return on his or her behalf. Treasury will mail refund

checks, assessments and all correspondence to the firm at the address indicated on the return. The firm must agree to be responsible for the payment of any additional tax, interest and penalties as finally determined. Issues involving the tax liability reported on a composite return will be resolved with the firm. In unusual circumstances, the department may contact the participants.

Attachments

Attach the following items to the composite return:

•A copy of pages 1, 2 and 3 of the U.S. 1065 or U.S. 1120S .

•A Michigan Schedule of Apportion- ment (Form

•All required forms

•Two schedules (one for participants and one for nonparticipants) listing each partner’s, shareholder’s or member's name, address, SSN and respective share of Michigan income and/or loss. If the participating member is another

•A statement signed by an authorized officer or general partner certifying that each participant has been informed of the terms and conditions of this program.

Lines not listed are explained on the form.

Line 10: Enter the apportionment percentage from Form

use the Single Business Tax apportionment percentage from Form

Line 13: The amount on this line should equal the total of lines 14, 15 and 16.

Line 21: Multiply the amount on line 20 by 3.95 percent (.0395).

Line 23: Enter the amount of withholding tax payments made on behalf of participating members.

The amount of withholding is calculated and remitted on a quarterly basis by multiplying the share of taxable income allocable to each member, adjusted for the allowable exemption amount for a quarter, times the income tax rate (4.0 percent through June 30, 2004 and 3.9 percent beginning July 1, 2004).

A

2004 807, PAGE 4

nonresident

Line 24: If line 22 plus line 23 is less than line 21, enter the balance of the tax due. This is the tax owed with the return. Enter any applicable penalties and interest in the spaces provided. Add tax, penalty and interest together and enter the total on this line. If balance due is less than $1, no payment is required. Make checks payable to “State of Michigan.” Write the firm’s FEIN, “Composite Return,” and the tax year on the front of the check. To ensure accurate processing of your return, send one check for each return type.

Line 27: Refund. Subtract line 26 from line 25. This is the refund. Treasury will not refund amounts less than $1.

Mail your completed return with payment (if applicable) to:

Composite Return

Michigan Department of Treasury

P.O. Box 30058

Lansing, MI 48909

Additions

Distributive Income Worksheet

Column A refers to Distributive Income categories from Schedule(s) K. Column B and C refer to lines on the U.S. 1065 Schedule K and U.S. 1120S Schedule K. Column D is the list of amounts that are added to arrive at total distributive income that is reported on Form 807, line 47.

A |

B |

|

C |

D |

U.S. 1065 |

|

U.S. 1120S |

Distributive Income |

|

Distributive Income Categories |

|

|||

Schedule K |

|

Schedule K |

Amounts |

|

|

|

|||

Ordinary income (loss) from trade or business |

1 |

|

1 |

|

activity |

|

|

||

|

|

|

|

|

Net income (loss) from rental real estate |

2 |

|

2 |

|

activity |

|

|

||

|

|

|

|

|

Net income (loss) from other rental activity |

3c |

|

3c |

|

|

|

|

|

|

Portfolio income (loss): |

|

|

|

|

Interest income |

5 |

|

4 |

|

|

|

|

|

|

Dividend income |

6a and 6b |

|

5a and 5b |

|

|

|

|

|

|

Royalty income |

7 |

|

6 |

|

|

|

|

|

|

Net |

8 |

|

7 |

|

|

|

|

|

|

Net |

9a |

|

8a |

|

|

|

|

|

|

Guaranteed payments |

4 |

|

|

|

|

|

|

|

|

Net gain (loss) under section 1231 |

10 |

|

9 |

|

|

|

|

|

|

Other income (loss) |

11 |

|

10 |

|

|

|

|

|

|

TOTAL DISTRIBUTIVE INCOME |

|

|

|

|

Add all amounts in Column D and carry total to Form 807, line 47. |

|

|

||

Lines 28 through 32: Enter income from lines 2, 3c, 4, 5a, 5b, 6, 7, 8a, 9 and 10 of 1120S Schedule K and from lines 2, 3c, 5, 6a, 6b, 7, 8, 9a, 10 and 11 of U.S. 1065 Schedule K. Guaranteed payments, income attributable to other Michigan fiduciaries or

Line 33: Enter the amount of state and local income taxes that was used to determine ordinary income on line 22 of the U.S. 1065 or line 21 of the U.S. 1120S.

Line 34: Enter other additions to income, such as gross interest and dividends from obligations or securities of states and their political subdivisions other than Michigan.

Subtractions

Note: Charitable contributions and other amounts reported as itemized deductions on U.S. SCHEDULE A are not allowable subtractions in determining Michigan taxable income.

Line 36: Enter income (loss) from other fiduciaries or other

income. Attach a schedule showing the location of companies and amount of income attributable to each.

Line 37: Enter amounts such as interest from U.S. obligations that are included in line 30a, and other deductions for AGI (above the line) that were not included in determining ordinary income. This includes section 179 depreciation and amounts included on line 12[d][2] of U.S. 1120S Schedule K and on line 13[d][2] of U.S. 1065 Schedule K. Attach a schedule of all subtractions.

Michigan allocated income or loss

Line 39: Enter the portion of guaranteed payments attributable to services performed in Michigan by the nonresident participants.

Line 40: Enter income from other fiduciaries or other

Line 41: Enter gains/losses from the sale of real or personal property located in Michigan not subject to apportionment.

Line 42: Enter any other income (loss) allocated to Michigan. Include any Michigan net operating loss deduction (NOLD). Partnerships may include the Section 179 expenses on property located in Michigan as a deduction here. Attach schedules.

Exemption Allowance

Line 47: Enter the total distributive income as determined using the worksheet on this page.

Line 48: Compute the percentage of income attributable to Michigan by dividing total Michigan income (line 46) by the total distributive income (line 47). This figure may not exceed 100 percent.

SEP, SIMPLE or qualified plan subtractions

SEP - Simplified Employee Pensions

SIMPLE - Savings Incentive Match Plan for Employees

Line 50: Figure the portion of SEP, SIMPLE or qualified plan subtractions which is attributable to the participants. Attach a schedule showing calculations.

The Michigan 807 form, which is a composite individual income tax return, shares similarities with several other tax documents. Each of these forms serves specific purposes in reporting income and tax obligations, particularly for partnerships and flow-through entities. Below is a list of eight documents that are similar to the Michigan 807 form, along with explanations of their similarities:

Understanding these documents can help streamline the tax filing process for partnerships and S Corporations operating in Michigan. Each form plays a crucial role in ensuring compliance with tax regulations while accurately reflecting the financial activities of the entities involved.

Michigan Tax Brackets 2023 - Taxpayers adjust withholding amounts based on total Michigan payroll reported.

If you are looking for a detailed guide on creating your own residential Lease Agreement, it is important to understand the key aspects of the document. This form will help both landlords and tenants clarify their rights and obligations. For more information, visit our resources on the subject, including a thorough overview of the Lease Agreement process.

Michigan Molina Prior Authorization - Specific details about the referred provider, including their name and address, are required.

Mi-1040 Form 2023 - You can submit your completed form via fax or traditional mail to the Michigan Department of Treasury.

Understanding the Michigan 807 form can be challenging, and several misconceptions often arise. Here are seven common misunderstandings:

This form is actually designed for flow-through entities, such as partnerships and S corporations, that have nonresident members. It allows these entities to report income on behalf of their members.

In fact, the Michigan 807 form requires several attachments, including pages from the U.S. 1065 or 1120S and a list of participants. Failing to include these can lead to processing delays.

Not all members can participate. For example, members claiming certain credits or who are Michigan residents cannot be included in the composite return.

The due date can vary. For the 2004 tax period, the return was due on April 15, 2005. Always check for the specific year you are filing.

Entities must make estimated tax payments on behalf of nonresident members. These payments are due quarterly, regardless of the composite return.

Calculations are essential. You must determine ordinary income, additions, subtractions, and apportionment percentages to complete the form accurately.

Failing to file on time can result in penalties and interest. It's crucial to either file by the deadline or request an extension in advance.

Completing the Michigan 807 form requires careful attention to detail and accurate reporting of income and deductions. This form is due on April 15, 2005, for tax periods ending in 2004. Before starting, gather all necessary documents, including the U.S. 1065 or 1120S forms, and any supporting schedules. Ensure that you have the required information for all participants in the composite return.

When filling out the Michigan 807 form, it's important to follow specific guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do: