Fill Your Michigan C 8000H Template

Michigan PDF Forms

Fill Your Michigan C 8000H Template

The Michigan C 8000H form is a crucial document for businesses seeking to calculate their single business tax apportionment percentage. However, it is often used in conjunction with several other forms and documents that help ensure compliance with state tax regulations. Below are four additional forms that are commonly associated with the C 8000H form.

Using these forms in conjunction with the Michigan C 8000H ensures that businesses accurately report their tax obligations and comply with state regulations. Understanding each form's purpose and requirements can help streamline the filing process and avoid potential issues with tax authorities.

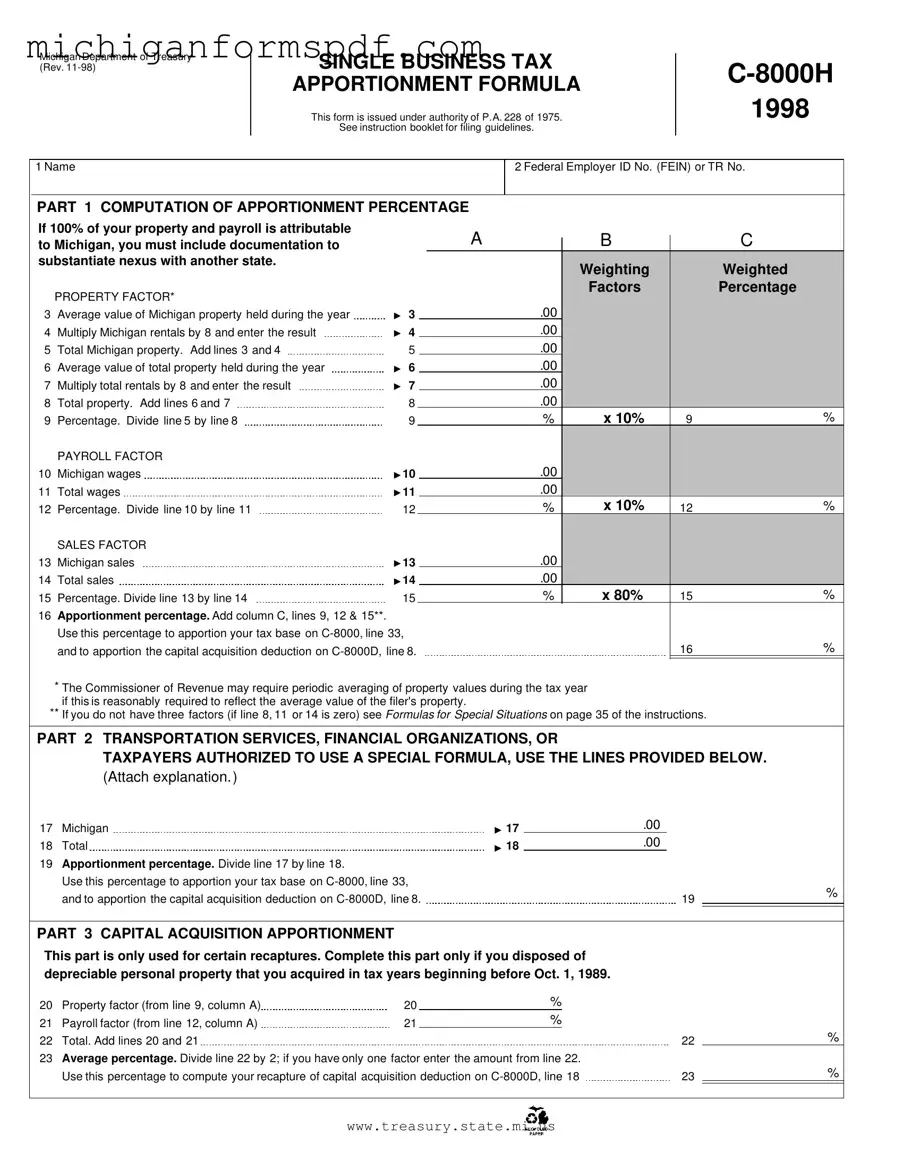

Michigan Department of Treasury (Rev.

SINGLE BUSINESS TAX APPORTIONMENT FORMULA

This form is issued under authority of P.A. 228 of 1975.

See instruction booklet for filing guidelines.

1998

1 Name

2 Federal Employer ID No. (FEIN) or TR No.

PART 1 COMPUTATION OF APPORTIONMENT PERCENTAGE

If 100% of your property and payroll is attributable |

|

|

|

|

A |

|

B |

|

C |

|

to Michigan, you must include documentation to |

|

|

|

|

|

|

||||

substantiate nexus with another state. |

|

|

|

|

|

|

Weighting |

|

Weighted |

|

|

|

|

|

|

|

|

|

|

||

|

PROPERTY FACTOR* |

|

|

|

|

|

|

Factors |

|

Percentage |

|

|

|

|

|

|

|

|

|

|

|

3 |

Average value of Michigan property held during the year |

▼ |

3 |

|

|

|

.00 |

|

|

|

4 |

Multiply Michigan rentals by 8 and enter the result |

▼ |

4 |

|

|

|

.00 |

|

|

|

5 |

Total Michigan property. Add lines 3 and 4 |

|

5 |

|

|

|

.00 |

|

|

|

6 |

Average value of total property held during the year |

▼ |

6 |

|

|

|

.00 |

|

|

|

7 |

Multiply total rentals by 8 and enter the result |

▼ |

7 |

|

|

|

.00 |

|

|

|

8 |

Total property. Add lines 6 and 7 |

|

8 |

|

|

|

.00 |

|

|

|

9 |

Percentage. Divide line 5 by line 8 |

|

9 |

|

|

|

% |

x 10% |

9 |

% |

|

PAYROLL FACTOR |

|

|

|

|

|

|

|

|

|

10 |

Michigan wages |

▼ |

10 |

|

|

|

.00 |

|

|

|

11 |

Total wages |

▼ |

11 |

|

|

|

.00 |

|

|

|

12 |

Percentage. Divide line 10 by line 11 |

|

12 |

|

|

|

% |

x 10% |

12 |

% |

|

SALES FACTOR |

|

|

|

|

|

|

|

|

|

13 |

Michigan sales |

▼ |

13 |

|

|

|

.00 |

|

|

|

14 |

Total sales |

▼ |

14 |

|

|

|

.00 |

|

|

|

15 |

Percentage. Divide line 13 by line 14 |

|

15 |

|

|

|

% |

x 80% |

15 |

% |

16 |

Apportionment percentage. Add column C, lines 9, 12 & 15**. |

|

|

|

|

|

|

|

|

|

|

Use this percentage to apportion your tax base on |

|

|

|

|

|||||

|

and to apportion the capital acquisition deduction on |

|

|

16 |

% |

|||||

|

|

|

|

|

|

|

|

|

|

|

*The Commissioner of Revenue may require periodic averaging of property values during the tax year if this is reasonably required to reflect the average value of the filer's property.

**If you do not have three factors (if line 8, 11 or 14 is zero) see Formulas for Special Situations on page 35 of the instructions.

PART 2 TRANSPORTATION SERVICES, FINANCIAL ORGANIZATIONS, OR

TAXPAYERS AUTHORIZED TO USE A SPECIAL FORMULA, USE THE LINES PROVIDED BELOW.

(Attach explanation. )

17 Michigan

▼

17

.00

18Total

19Apportionment percentage. Divide line 17 by line 18.

Use this percentage to apportion your tax base on

▼

18

.00

19 |

% |

|

PART 3 CAPITAL ACQUISITION APPORTIONMENT

This part is only used for certain recaptures. Complete this part only if you disposed of depreciable personal property that you acquired in tax years beginning before Oct. 1, 1989.

20 |

Property factor (from line 9, column A) |

20 |

% |

|

|

|

21 |

Payroll factor (from line 12, column A) |

21 |

% |

|

|

|

22 |

Total. Add lines 20 and 21 |

|

|

|

22 |

% |

23 |

Average percentage. Divide line 22 by 2; if you have only one factor enter the amount from line 22. |

|

|

|||

|

Use this percentage to compute your recapture of capital acquisition deduction on |

23 |

% |

|||

www.treasury.state.mi.us

The Michigan C 8000H form is a crucial document for businesses operating in Michigan, specifically for calculating the apportionment percentage for the Single Business Tax. Several other forms share similarities with the C 8000H in their purpose or structure. Here are seven documents that are comparable to the Michigan C 8000H form:

Each of these forms plays a role in tax reporting and apportionment, similar to the Michigan C 8000H. Understanding their connections can help ensure compliance and accurate tax calculations.

Michigan Nonprofit - Check all provided contacts and addresses to ensure they are updated and accurate for better communication.

For those navigating the complexities of workers' compensation in Georgia, it is important to understand the significance of the Georgia WC-14 form. This essential document is designed to notify the Georgia State Board of Workers' Compensation about claims related to workplace injuries. Employees can formally submit a claim or request a hearing or mediation to ensure their rights are protected. To find further guidance and resources, you can visit Forms Georgia, where additional information is available to assist in the timely completion and submission of the WC-14 form, which is crucial for efficient claim processing.

Michigan Permit - Employers must post required workplace posters related to youth employment laws visibly at the workplace.

Here are nine common misconceptions about the Michigan C 8000H form, along with clarifications to help you better understand its purpose and requirements.

This form applies to all businesses subject to the Single Business Tax in Michigan, regardless of size.

If your business has property or payroll in Michigan, you must file the form to apportion your tax base, even if all operations are within the state.

The apportionment percentage varies based on the property, payroll, and sales factors, which must be calculated accurately.

This form can also apply to businesses that disposed of depreciable personal property acquired in tax years before that date.

It is crucial to follow the instructions provided with the form to ensure compliance and avoid errors in your calculations.

All three factors—property, payroll, and sales—are essential for determining the overall apportionment percentage.

If any of the factors have zero values, you must refer to the "Formulas for Special Situations" in the instructions for guidance on how to proceed.

Documentation is required to substantiate nexus with other states if 100% of your property and payroll is attributed to Michigan.

In addition to the C 8000H, businesses may need to complete other forms, such as the C-8000, depending on their specific tax situations.

Completing the Michigan C 8000H form is essential for determining your apportionment percentage for the Single Business Tax. Follow these steps carefully to ensure accurate submission. Gather all necessary financial documents before you begin, as you will need them to fill in the required information.

After completing the form, double-check all entries for accuracy. Ensure that you have all supporting documentation ready for submission. This will help avoid any delays in processing your form. Once verified, submit the form as directed in the instruction booklet.

When filling out the Michigan C 8000H form, it is essential to follow certain guidelines to ensure accuracy and compliance. Here are seven key do's and don'ts: