Fill Your Michigan Property Transfer Affidavit 2766 Template

Michigan PDF Forms

Fill Your Michigan Property Transfer Affidavit 2766 Template

The Michigan Property Transfer Affidavit 2766 form is a crucial document used during real estate transactions in Michigan. To ensure a smooth transfer of property ownership, several other forms and documents are often required. Below is a list of related documents that may accompany the Property Transfer Affidavit.

Understanding these documents is essential for both buyers and sellers. Each plays a significant role in the property transfer process, ensuring that all legal requirements are met and protecting the interests of all parties involved.

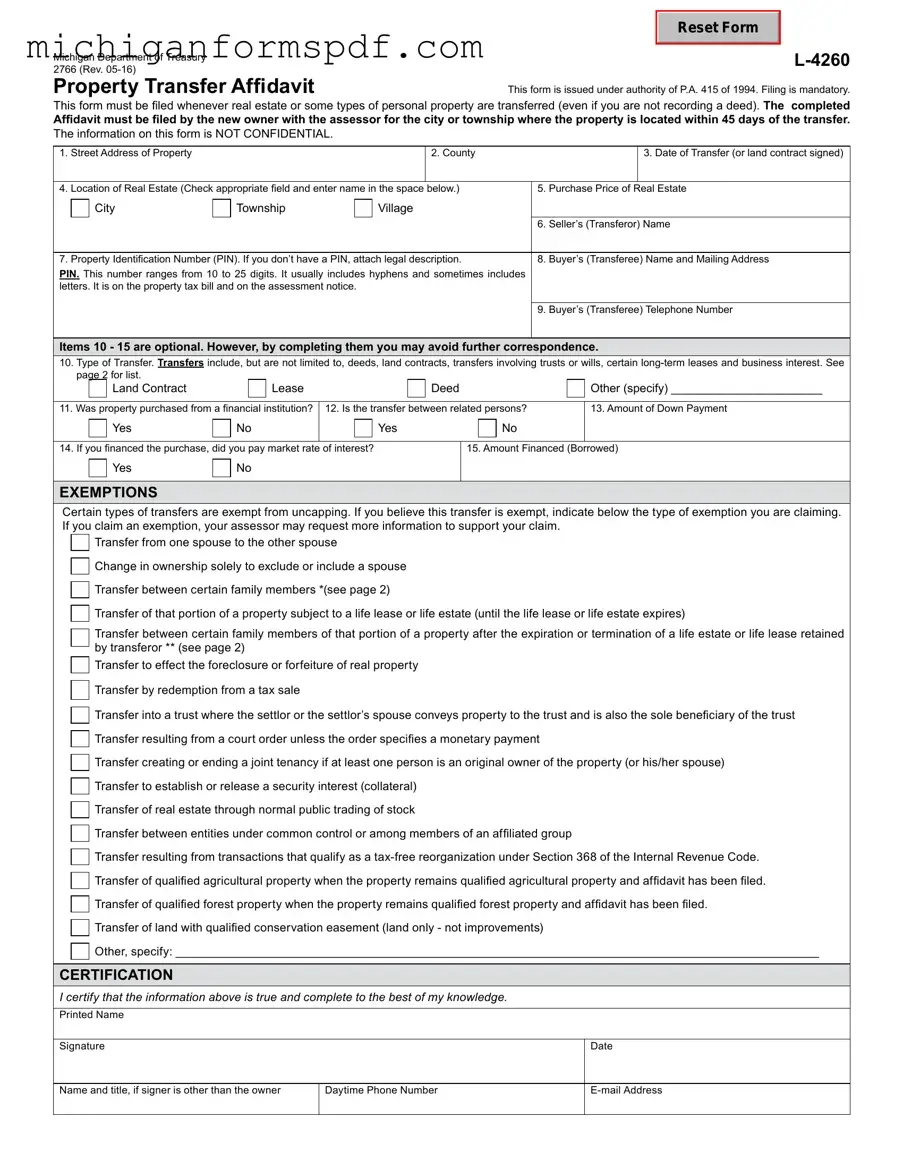

Reset Form

This form is issued under authority of P.A. 415 of 1994. Filing is mandatory.

This form must be filed whenever real estate or some types of personal property are transferred (even if you are not recording a deed). The completed

Affidavit must be filed by the new owner with the assessor for the city or township where the property is located within 45 days of the transfer. The information on this form is NOT CONFIDENTIAL.

1. |

Street Address of Property |

|

|

|

|

2. County |

|

|

3. Date of Transfer (or land contract signed) |

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Location of Real Estate (Check appropriate field and enter name in the space |

below.) |

5. |

Purchase Price of |

Real Estate |

|||||

|

|

City |

|

Township |

|

Village |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

6. |

Seller’s (Transferor) Name |

|

|

|

|

|

|

|

|

|

|

|

|

7. |

Property Identification Number (PIN). If you don’t have a PIN, attach legal description. |

8. |

Buyer’s (Transferee) Name and Mailing Address |

|||||||

PIN. This number ranges from 10 to 25 digits. It usually includes hyphens and sometimes includes |

|

|

|

|||||||

letters. It is on the property tax bill and on the assessment notice. |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

Buyer’s (Transferee) Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

|

Items 10 - 15 are optional. However, by completing them you may avoid further correspondence.

10.Type of Transfer. Transfers include, but are not limited to, deeds, land contracts, transfers involving trusts or wills, certain

|

|

Land Contract |

|

|

|

Lease |

|

|

|

|

Deed |

|

Other (specify) _______________________ |

|||

|

|

|

|

|

||||||||||||

11. Was property purchased from a financial institution? |

12. Is the transfer between related persons? |

|

13. Amount of Down Payment |

|||||||||||||

|

|

Yes |

|

No |

|

|

Yes |

|

|

|

|

No |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|||||||||||

14. If you financed the purchase, did you pay market rate |

of interest? |

|

|

15. Amount Financed (Borrowed) |

||||||||||||

|

|

Yes |

|

No |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EXEMPTIONS

Certain types of transfers are exempt from uncapping. If you believe this transfer is exempt, indicate below the type of exemption you are claiming. If you claim an exemption, your assessor may request more information to support your claim.

Transfer from one spouse to the other spouse

Change in ownership solely to exclude or include a spouse

Transfer between certain family members *(see page 2)

Transfer of that portion of a property subject to a life lease or life estate (until the life lease or life estate expires)

Transfer between certain family members of that portion of a property after the expiration or termination of a life estate or life lease retained by transferor ** (see page 2)

Transfer to effect the foreclosure or forfeiture of real property

Transfer by redemption from a tax sale

Transfer into a trust where the settlor or the settlor’s spouse conveys property to the trust and is also the sole beneficiary of the trust Transfer resulting from a court order unless the order specifies a monetary payment

Transfer creating or ending a joint tenancy if at least one person is an original owner of the property (or his/her spouse)

Transfer to establish or release a security interest (collateral)

Transfer of real estate through normal public trading of stock

Transfer between entities under common control or among members of an affiliated group

Transfer resulting from transactions that qualify as a

Transfer of land with qualified conservation easement (land only - not improvements)

Other, specify: __________________________________________________________________________________________________

CErTIfICaTION

I certify that the information above is true and complete to the best of my knowledge.

Printed Name

Signature

Date

Name and title, if signer is other than the owner

Daytime Phone Number

2766, Page 2

Instructions:

This form must be filed when there is a transfer of real property or one of the following types of personal property:

•Buildings on leased land.

•Leasehold improvements, as defined in MCL Section 211.8(h).

•Leasehold estates, as defined in MCL Section 211.8(i) and (j).

Transfer of ownership means the conveyance of title to or a present interest in property, including the beneficial use of the property. For complete descriptions of qualifying transfers, please refer to MCL Section

Excerpts from Michigan Compiled Laws (MCL), Chapter 211

**Section 211.27a(7)(d): Beginning December 31, 2014, a transfer of that portion of residential real property that had been subject to a life estate or life lease retained by the transferor resulting from expiration or termination of that life estate or life lease, if the transferee is the transferor’s or transferor’s spouse’s mother, father, brother, sister, son, daughter, adopted son, adopted daughter, grandson, or granddaughter and the residential real property is not used for any commercial purpose following the transfer. Upon request by the department of treasury or the assessor, the transferee shall furnish proof within 30 days that the transferee meets the requirements of this subdivision. If a transferee fails to comply with a request by the department of treasury or assessor under this subdivision, that transferee is subject to a fine of $200.00.

*Section 211.27a(7)(u): Beginning December 31, 2014, a transfer of residential real property if the transferee is the transferor’s or the transferor’s spouse’s mother, father, brother, sister, son, daughter, adopted son, adopted daughter, grandson, or granddaughter and the residential real property is not used for any commercial purpose following the conveyance. Upon request by the department of treasury or the assessor, the transferee shall furnish proof within 30 days that the transferee meets the requirements of this subparagraph. If a transferee fails to comply with a request by the department of treasury or assessor under this subparagraph, that transferee is subject to a fine of $200.00.

Section 211.27a(10): “... the buyer, grantee, or other transferee of the property shall notify the appropriate assessing office in the local unit of government in which the property is located of the transfer of ownership of the property within 45 days of the transfer of ownership, on a form prescribed by the state tax commission that states the parties to the transfer, the date of the transfer, the actual consideration for the transfer, and the property’s parcel identification number or legal description.”

Section 211.27(5): “Except as otherwise provided in subsection (6), the purchase price paid in a transfer of property is not the presumptive true cash value of the property transferred. In determining the true cash value of transferred property, an assessing officer shall assess that property using the same valuation method used to value all other property of that same classification in the assessing jurisdiction.”

Penalties:

Section 211.27b(1): “If the buyer, grantee, or other transferee in the immediately preceding transfer of ownership of property does not notify the appropriate assessing office as required by section 27a(10), the property’s taxable value shall be adjusted under section 27a(3) and all of the following shall be levied:

(a)Any additional taxes that would have been levied if the transfer of ownership had been recorded as required under this act from the date of transfer.

(b)Interest and penalty from the date the tax would have been originally levied.

(c)For property classified under section 34c as either industrial real property or commercial real property, a penalty in the following amount:

(i)Except as otherwise provided in subparagraph (ii), if the sale price of the property transferred is $100,000,000.00 or less, $20.00 per day for each separate failure beginning after the 45 days have elapsed, up to a maximum of $1,000.00.

(ii)If the sale price of the property transferred is more than $100,000,000.00, $20,000.00 after the 45 days have elapsed.

(d)For real property other than real property classified under section 34c as industrial real property or commercial real property, a penalty of $5.00 per day for each separate failure beginning after the 45 days have elapsed, up to a maximum of $200.00.

Quit Claim Deed: This document transfers ownership of property from one party to another without any warranties. Like the Property Transfer Affidavit, it is often used in situations where the transfer is between family members or in divorce settlements.

Warranty Deed: This form guarantees that the seller has clear title to the property and the right to sell it. Similar to the Property Transfer Affidavit, it is used to formally document the transfer of property ownership.

Real Estate Purchase Agreement: This contract outlines the terms of a sale between a buyer and a seller. While it serves a different purpose, it also plays a crucial role in the property transfer process, just like the Property Transfer Affidavit.

Affidavit of Title: This document confirms the seller's ownership and the absence of liens on the property. It complements the Property Transfer Affidavit by providing additional assurance to the buyer about the property's status.

Transfer on Death Deed: This allows an individual to transfer property to a beneficiary upon their death without going through probate. Like the Property Transfer Affidavit, it facilitates a smooth transition of property ownership.

2022 Michigan Tax Forms - Filers can opt to have Treasury compute their interest instead of completing the form.

How Old Do You Have to Be to Take a Ged Test - Consider mailing your request to ensure it reaches the appropriate department.

For those interested in drafting a legal document, a helpful resource is available at promissoryform.com/blank-nevada-promissory-note, which provides a template that can guide you in creating a Nevada Promissory Note, ensuring that all essential details are accurately captured and facilitating a clear understanding between the involved parties.

Form 1098 Mortgage - The form must be submitted with a $10 application fee.

The Michigan Property Transfer Affidavit 2766 form is an important document in real estate transactions. However, several misconceptions about this form can lead to confusion. Here are six common misunderstandings:

Understanding these misconceptions can help ensure compliance with Michigan's property transfer regulations. Properly completing and filing the affidavit is crucial for a smooth transaction.

Completing the Michigan Property Transfer Affidavit 2766 form is an important step in the property transfer process. After filling out the form, it should be submitted to the appropriate local tax assessing office. This ensures that the transfer is properly recorded and that any necessary tax assessments can be made.

When filling out the Michigan Property Transfer Affidavit 2766 form, it's essential to be thorough and accurate. Here are five key things to consider: